Whether you’re a stock-market investor, an employee of a private business or a customer of one of the thousands of consumer-facing companies owned by private-equity funds, private equity is part of your life.

It’s a world that remains out of the spotlight much of the time, but one that has grown too big to ignore.

Assets under management have tripled to $12 trillion in less than a decade, making the world of alternative investments a significant part of the overall economy.

By comparison, the U.S. stock-market pantheon of 2,800 New York Stock Exchange stocks and 3,300 Nasdaq stocks tips the scales at a combined market capitalization of $46.2 trillion.

Outside of those roughly 6,000 listed companies on the Nasdaq and the NYSE, the world of private equity is a major player in the larger universe of private companies, often owned by families or other private-equity firms.

Private-equity firms are currently invested in about 14,300 companies in the U.S., according to industry estimates.

About 21,000 businesses in the U.S. have 500 or more employees, according to the Small Business & Entrepreneurship Council. Along with those larger companies, the U.S. currently supports more than 33 million small businesses employing 61.7 million people, according to the Small Business Administration.

That’s a very big sandbox outside of the smaller world of publicly traded companies.

To put the $12 trillion under management in alternative investments into further perspective:

- U.S. banks reported total combined assets under management of $23.47 trillion as of June 30.

- The U.S. Social Security Administration reported $2.83 trillion in trust-fund reserves in its 2023 report.

- Total U.S. retirement assets for the U.S. were $36.7 trillion, including $13 trillion in individual retirement accounts and $10.2 trillion in defined-contribution plans such as 401(k)s, as of June 30, according to the Investment Company Institute.

Private-equity firms are often involved in the birth of publicly traded companies by backing initial public offerings. They also lead take-private deals that end the life of public companies on the NYSE or Nasdaq when they buy all the common stock in a target business.

If you’re one of the roughly 19 million public employees in the U.S. working for a state or municipality, or if you work for a large learning institution, a chunk of your retirement plan’s money is invested in private-equity funds, private credit funds and other alternatives.

Nuts and bolts

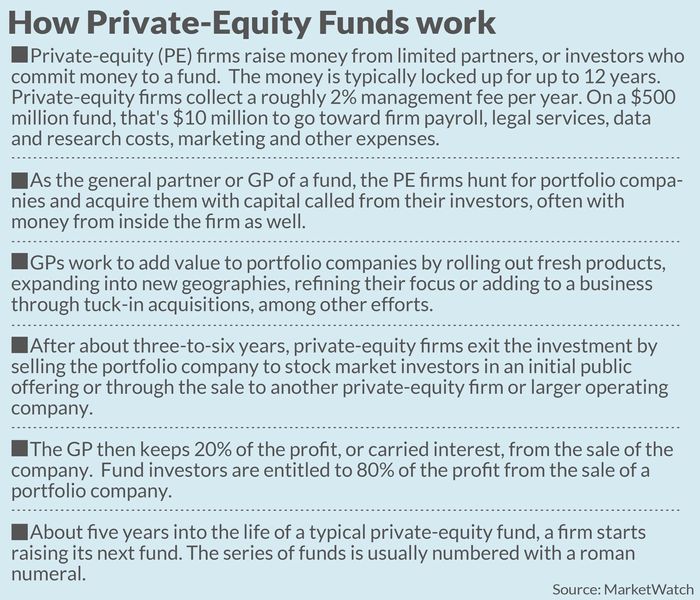

So what exactly is a private-equity fund and how does it work?

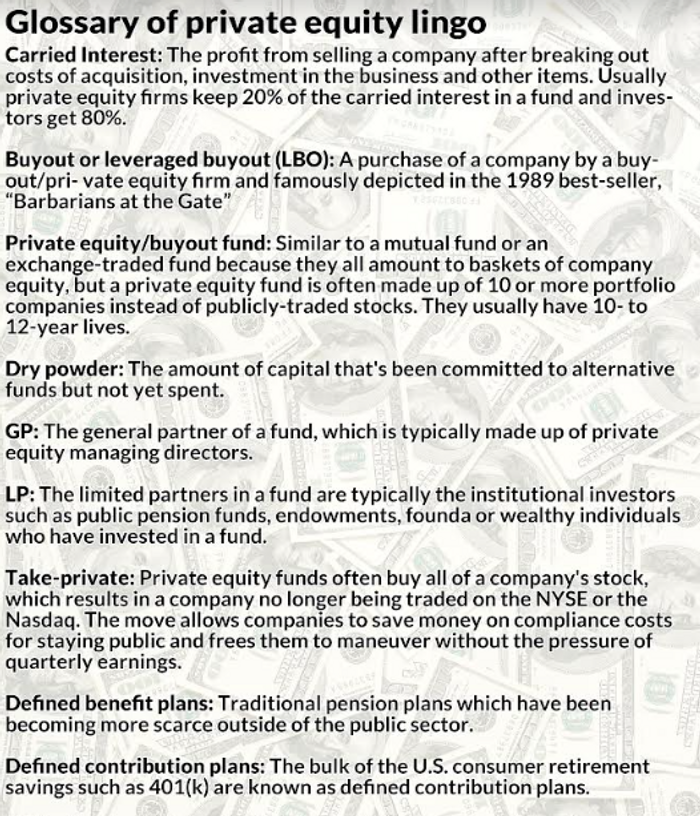

Not unlike an exchange-traded fund or a mutual fund, a private-equity fund holds a basket of companies. Traditional private-equity buyout funds are typically made up of 10 to 15 companies, versus the dozens or hundreds of companies in an ETF, say, for the S&P 500

SPX

or the Nasdaq-100.

Private-equity funds are also similar to stocks, because both stock owners and private-equity fund owners purchase equity in companies. Private credit funds resemble bonds in some ways, because both represent investments in debt.

Unlike money invested in stocks or bonds, however, money put into a fund is typically locked up for at least 10 years, although investors — also known as limited partners, or LPs for short — start getting some of their money back within a few years as the firm sells, or exits, its portfolio companies.

Early in the life of a fund, private-equity firms call in capital from their investors to buy companies. The firms typically own the companies for three to five years and then sell them.

Every time a sale happens, the LPs are entitled to 80% of any profit from the sale of the company. The private-equity fund’s general partners, or GPs — made up of private-equity executives — get 20% of the profit, which is called carried interest. By the end of the life of a fund, all the companies have been bought and sold, with cash dispersed to investors and the firm.

Once a firm deploys about 70% of the capital in a fund, about four to six years into the life of the fund, it starts raising capital for its next fund.

Another subset of the alternative investments has grown up around the sale of stakes in private-equity funds. If an investor wants to get out of a fund for whatever reason, that investor is often able to sell its stake to another investor on the secondary market. This has grown into a huge business in its own right, with massive secondary funds made up of many stakes in private-equity funds. In another twist, some investment shops buy up stakes in private-equity firms.

While private equity has been on Wall Street’s map as a separate practice since the 1980s, the industry was formerly known as merchant banking. Banks would invest off their own balance sheets to buy companies or other assets and would often line up investors either from within the bank or elsewhere to provide capital.

After the global financial crisis of 2007-08, many banks spun off their private-equity units into independent firms.

However, Goldman Sachs Group Inc.

GS,

has continued to run its merchant bank, which it folded into its Global Asset and Wealth Management unit.

Also read: Goldman Sachs’s private-equity business has been a ‘black box,’ but now it’s opening up

Image problem

To be sure, the private-equity business is not always portrayed in a favorable light. Books such as the 1989 bestseller “Barbarians at the Gate” by Bryan Burrough and John Helyar, or the recently released “These Are the Plunderers” by New York Times writer Gretchen Morgenson and financial-policy analyst Joshua Rosner, portray a world of wheeling and dealing by greedy executives who are enriching themselves with little regard for the workers at the companies they target. The titles of the books alone say as much.

Private-equity firms may make a lot of money, but they do a lot better when their portfolio companies thrive from their investments, and not from looting them.

Some private-equity executives have complained that the industry has an image problem — one that venture capitalists have mostly managed to avoid by positioning themselves as thought leaders and trend setters by investing in hot startups.

Others point out that the industry shows merit because it’s had a solid track record of stewardship for major pension funds and other institutional investors.

“I disagree that private equity has a general, across-the-board image problem,” said Kelly DePonte, managing director of Probitas Partners, a placement firm that helps alternative-investment managers raise capital. “There are certainly bad actors in the industry — as there are in all industries — and certain academics and politicians are negatively focused on fees. But many investors look at returns net of fees as attractive, especially compared to other investments over the past decade.”

But there’s no question that the riches made in the industry may cause some to wonder whether the industry plays a fair game.

Among the wealthiest executives in the U.S., Stephen Schwarzman, chief executive of the largest publicly traded private-equity firm, Blackstone Inc.

BX,

earned about $1 billion in dividends from his company’s stock plus about $251 million in compensation in 2022 alone. Forbes magazine estimates his current net worth at about $35 billion.

By contrast, BlackRock Inc.

BLK,

Chief Executive Larry Fink, who runs the largest asset manager in the world, with assets under management of $9.4 trillion, is worth about $1 billion, according to Forbes.

Private equity has mostly kept a low profile, with few household names in the business.

When Mitt Romney, co-founder of large private-equity firm Bain Capital, ran for president against Barack Obama in 2008, he famously said, “I like being able to fire people.” Romney made the remark in the context of his healthcare platform, as he explained how it’s a good thing for people to be able to switch service providers if those providers are not meeting their needs, but the comment was often cited as an interpretation of his job as a private-equity executive.

One of the only highly visible people in the world of private equity right now is reality TV star Kim Kardashian. She is currently at the helm of Skky Partners, a firm she co-founded with Carlyle Group Inc.

CG,

veteran Jay Sammons that’s taking aim at investments in fashion, media, beauty, media, hospitality and food.

Politicians including Democratic Sen. Elizabeth Warren have criticized private-equity firms as loading up their portfolio companies with debt and then laying off workers. In 2021, Warren filed a bill called the Stop Wall Street Looting Act, but the legislation has never made it out of Congress.

Instead, private-equity firms last year managed to keep carried interest taxed at the same level as capital gains rather than as income, a move that saved the industry tens of billions of dollars in potential tax increases.

Also read: We expect it to be removed’: Democrats’ push to close ‘carried interest loophole’ in jeopardy as Sinema seeks to block effort

Stewards of capital for retirement funds

While private equity has a reputation for excessive profits and “looting” on one side, pension funds and other managers of retirement capital have been pouring more and more money into the asset class.

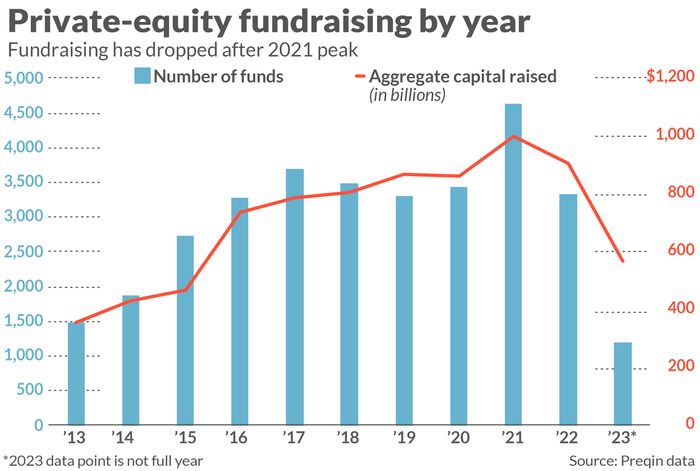

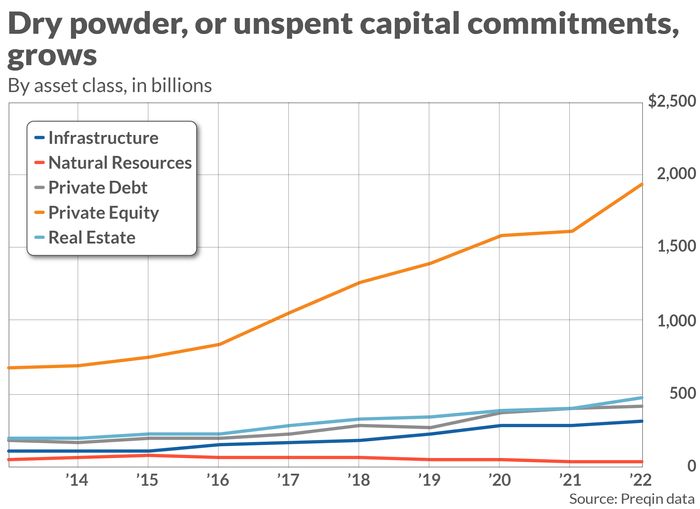

The money raised by private-equity funds peaked at more than $1.1 trillion in 2021. While it has been affected by rocky financial markets in 2022 and 2023, the industry still has more money than it has been able to deploy.

Private-equity firms often face an issue that few would consider a problem: too much money waiting to be put to work. This cache of so-called dry powder rose to nearly $2 trillion in 2022.

At last check, about 12 million people in the U.S. work for companies backed by private-equity firms, and they earn an estimated $1 trillion in wages, according to data from the American Investment Council, a trade group for private-equity firms. The entire U.S. private-equity sector accounts for about 6.5% of U.S. gross domestic product, or about $1.7 trillion, according to the AIC.

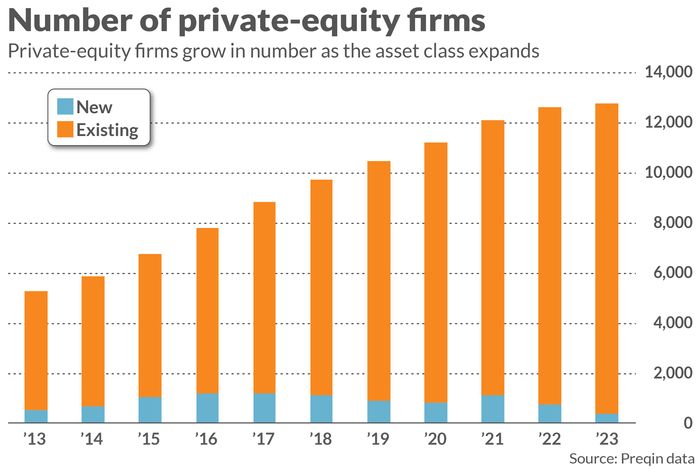

The total number of private-equity firms topped 12,000 at last check, up from fewer than 6,000 in 2013, according to investment-data company Preqin.

While the median business backed by private equity has 69 workers, many larger, widely known companies such as Uber Technologies Inc.

UBER,

Airbnb Inc.

ABNB,

Yeti Holdings Inc.

YETI,

Dunkin, Safeway, PetSmart, Hilton Hotels, Toys R Us, RJR Nabisco and Kinder Morgan have been backed by private-equity firms.

If you own stock, you’ve probably seen some of your publicly traded companies being gobbled up by take-private leveraged-buyout deals led by private-equity firms. A historic case would be KKR & Co.’s

KKR,

$25 billion buyout of RJR Nabisco, which put private equity firmly on Wall Street’s radar in 1988 as one of the largest-ever mergers at the time.

A fresher example is that of retailer Chico FAS

CHS,

which is being acquired for $1 billion by Sycamore Partners, a private-equity firm that manages a portfolio of retail brands such as Staples, Hot Topic, the Limited, Talbots, Dollar Express and Nine West.

This transaction type has drawn criticism because leveraged buyouts often involve loading up the target company with expensive debt. If the company manages to match growth projections at the time of the deal, this is not usually a problem.

In some cases, however, a particular industry or an individual company could fall on hard times, leaving private-equity portfolio companies with weak balance sheets or facing bankruptcy.

One high-profile example was the buyout of Toys R Us, which was acquired for $7.5 billion by Bain Capital, Vornado Realty Trust and KKR & Co. in 2005. Prior to the deal, Toys R Us had less than $2 billion in debt, but after the deal closed, that figure grew to $5 billion.

Impacted by steep debt payments and competition from retailing giants such as Walmart Inc.

WMT,

and online competitors such as Amazon.com Inc.

AMZN,

Toys R Us went bankrupt, resulting in about 33,000 layoffs in 2018.

Employees at Toys R Us won a $2 million severance settlement a year later, while separately, KKR & Co. and Bain Capital committed a combined $20 million to launch the TRU Financial Assistance Fund in late 2018.

Such a move would have gained support from one of the biggest investor groups in private-equity funds, public pension funds.

Several private-equity firms are publicly traded

While public pension funds and other institutional investors continue to plow money into alternative investments, most 401(k) plans for individuals are not tapping into private equity.

For now, private-equity firms continue to expand their reach to individuals mostly through the registered investment adviser network for moderately to extremely wealthy individuals with at least $1 million in assets outside of their primary home.

A specific type of fund called a 40 Act Fund is a publicly filed vehicle that invests money from individuals into private equity. One larger example of this fund type is the Partners Group Private Equity (Master Fund) LLC, with $13.6 billion in net assets for the fiscal year that ended March 31.

Getting access to the funds themselves allows investors to gain from the roughly 80% of the profit of buyout and other deals.

When you buy stock in a private-equity firm, the stock’s value is partly based on the 20% carried interest that the management company gets on private-equity deals, not on the lion’s share of the profits.

But if the 20% will suffice, individual investors may buy shares of several private-equity firms with stock listings in the U.S.

Blackstone Inc. was the first major U.S. private-equity firm to go public, in 2007. Nowadays, stocks are available from many other major firms, including Brookfield Corp

BN,

Apollo Global Management Inc.

APO,

Carlyle Group Inc.

CG,

KKR, TPG Inc.

TPG,

and others.

Many of the largest private-equity firms, however, are not publicly traded. Some of those include Thoma Bravo, GTCR, Lone Star Funds, Bain Capital, Vista Equity Partners, Global Infrastructure Partners, TA Associates, Warburg Pincus, General Atlantic, Advent International, Cerberus Capital Management, Fifth Street and Silver Lake.

Many specialty finance stocks, such as business-development companies, lend to private companies or take part in other alternative businesses. Some examples of lenders include Ares Management Corp.

ARES,

FS KKR Capital Corp.

FSK,

and Blue Owl Capital Inc.

OWL,

Blue Owl also invests in ownership stakes in private-equity firms.

Other public companies with exposure to private markets include Hamilton Lane Inc.

HLNE,

StepStone Group Inc.

STEP,

and PJT Partners Inc.

PJT,

Many of these corporate private-equity firms have diversified beyond private-equity buyout funds into credit, secondary, real-estate and infrastructure funds, to name a few. Private-equity funds remain the largest component of that pie.

In a sign that private equity may be ready for prime time in terms of stock investing, Blackstone this year reached a couple of milestones: It hit $1 trillion of assets and was recently named a component of the S&P 500.

Other private-equity firms with publicly traded stock may soon join the S&P 500, so investors may be hearing more from the sector as time goes on.

Key to whether investor interest in private equity continues will be the performance of the asset class, which has been boosted by the past era of low interest rates, which ended last year with a series of rapid rate hikes by the U.S. Federal Reserve and other central banks.

“These low interest rates were a boon to private-equity investment volume and returns and hit the attractiveness of investment-grade bonds,” said DePonte of Probitas Partners. “On a going-forward basis, we are likely to see higher interest rates, returning more toward historical norms — with more stress on private-equity returns and leverage.”

Calpers is a fan of alternatives

Private-equity and other alternative investments have made up a significant portion of the retirement savings of 34 million people in the U.S., especially from public pension funds.

One of the largest examples is the California Public Employees’ Retirement System, or Calpers. About $59.7 billion of its assets under management, or 12.9% of its total portfolio of $463 billion, is invested in private equity, and $10.3 billion, or 2.2%, is invested in private debt.

As big as public pension funds are, they only account for about $7.7 trillion of U.S. retirement assets, which totaled $35.4 trillion as of March 31, according to figures from the Investment Company Institute.

As the largest single piece, individual retirement accounts account for $12.5 trillion, followed by $9.8 trillion for defined-contribution plans, including 401(k) plans.

For now, a large portion of the client business for private equity comes from the world of institutional investors, including public pension funds, endowments and foundations, sovereign-wealth funds and family offices.

Some wealthy individuals who meet the U.S. criteria for investing in private-equity funds as so-called accredited investors also take part.

The goal of these investors is to balance their portfolios of public stocks and bonds with private-market returns from the alternatives. Such holdings increase diversification by offering access to private companies that often grow at a faster rate than larger public companies.

A December 2022 study by the Georgetown University Center for Retirement Initiatives concluded that target-date funds with alternatives included produced “positive” benefits.

“The amount of annual retirement income that can be generated by converting a participant defined contribution [such as 401(k) plans] has the potential to improve by 17% in the expected case and by 11% in a worst-case or downside outcome,” according to the study’s executive summary.

Read the full article here